Executive Summary

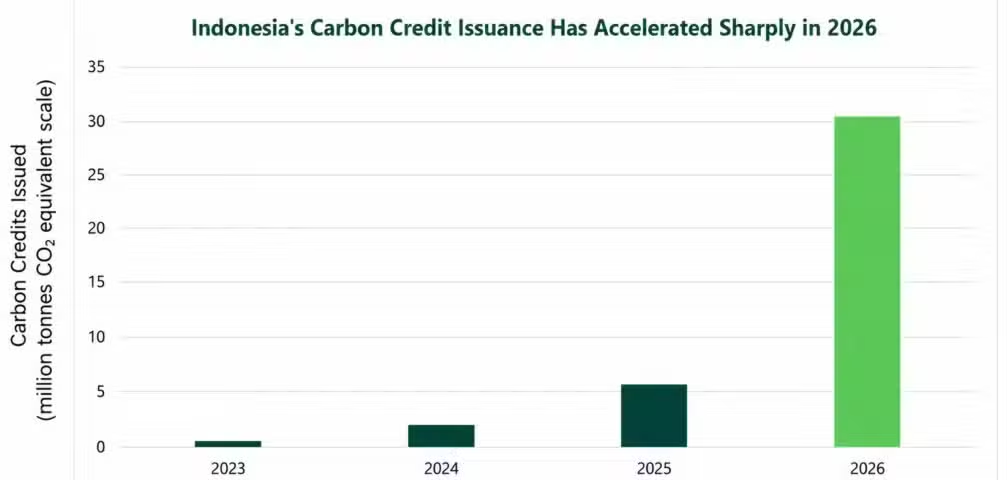

The month of July 2026 brought major changes to Indonesia’s carbon credit market. On July 6, 2026, the Ministry of Forestry approved four forestry carbon projects with an estimated emissions-reduction potential of more than 30 million tonnes CO₂e, clearing the way for associated carbon credits to be issued under Indonesia’s new forestry carbon framework. Three days later, on July 9, 2026, the Ministry of Environment switched on the Carbon Unit Registry System, known as SRUK. Singapore and Indonesia have also advanced a bilateral Article 6 partnership under the Paris Agreement. This framework lets Indonesian carbon credits count toward another country’s climate targets.

For a foreign investor, a domestic developer, or a board weighing its next climate investment, this is a major structural shift. Indonesia replaced its original 2021 carbon framework with a rebuilt regime under Presidential Regulation 110 of 2025. It also stopped the same carbon credit from being sold to two different buyers because of SRUK’s introduction. It then signed its first cross border deal under Article 6. And it did all this while holding one of the largest tropical forest estates on earth.

This guide explains what has changed and why it matters. It also sets out what a serious investor needs to know before committing capital. The following four points are the most critical:

- Indonesia closed several legal gaps that made foreign participation risky before 2025.

- The country’s national carbon balance remains a live political question. This means how much Indonesia can sell abroad without compromising its own climate targets.

- Forestry and land use dominate today’s market. Energy sector rules are still taking shape.

- The Singapore deal is very likely a template, not a one off. More bilateral agreements should follow before COP31.

Introduction to Carbon Credits

Indonesia sits at the heart of the Coral Triangle. It hosts the world’s largest mangrove ecosystems, the third largest tropical rainforest on the planet, and vast tropical peatlands. This natural endowment is not incidental to the carbon credit story. It is the reason Indonesia’s carbon market matters far beyond its own borders.

A carbon credit represents one tonne of carbon dioxide equivalent. A verifier confirms that a company has reduced, avoided, or removed this tonne from the atmosphere, measured against a defined baseline. A company that plants a forest, protects a peatland, or captures methane from a landfill can turn that reduction into a tradable unit. Buyers purchase these units to offset their own emissions or to meet a regulatory obligation.

Three distinct crediting bodies can generate a credit. A national government can run its own crediting mechanism, as Indonesia does through SPE-GRK. An independent private standard such as Verra, Gold Standard, or Plan Vivo can certify a project against its own methodology. Or a supranational body, namely the UNFCCC itself, can issue credits through its own mechanism under Article 6.4 of the Paris Agreement. Each route carries different costs, different timelines, and a different level of buyer recognition. Indonesia’s regulatory reforms in 2025 and 2026 now formally recognize all three.

Compliance Markets and Voluntary Markets

Global carbon markets split into two broad categories, though the line between them has blurred considerably in recent years. Compliance markets exist because a law requires certain companies to hold credits. The European Union’s emissions trading system works this way. Indonesia’s own Carbon Economic Value framework, known locally as Nilai Ekonomi Karbon or NEK, combines a carbon tax with an emissions trading scheme for coal fired power plants, and is a compliance market in this same sense. Voluntary markets exist because companies choose to buy credits, often to support a corporate sustainability commitment.

Treating these as entirely separate markets is a common mistake. A single credit generated by a single project can, depending on how it is authorized, serve a domestic compliance buyer, an international compliance scheme, or a voluntary corporate buyer. Getting this authorization decision right is exactly where a well structured legal and advisory relationship earns its value.

Article 6 and Why It Matters

Article 6 of the Paris Agreement adds a third layer that matters enormously for Indonesia. It lets one country transfer emission reductions to another. Both governments must agree, and both must apply what is called a corresponding adjustment. This adjustment stops both countries from claiming the same tonne of reduced carbon toward their own targets.

Article 6.2 covers bilateral and cooperative approaches between two countries, exactly the mechanism behind the Singapore partnership. Meanwhile, Article 6.4 creates a centralized United Nations mechanism, known as the Paris Agreement Crediting Mechanism, or PACM. PACM is not yet operational at scale. Regulators are still finalizing its rules, and the first PACM methodologies are expected for approval this year. Article 6.8 covers non-market approaches such as grants and technical cooperation.

Why does this distinction matter to an investor? A credit that has gone through a corresponding adjustment carries a different legal character than one that has not. Consequently, it often carries a different price too. So buyers seeking Article 6 compliant credits need certainty on this point before they commit funds. This is especially true for buyers facing carbon border taxes such as the European Union’s Carbon Border Adjustment Mechanism, or CBAM. It also matters for buyers subject to international compliance schemes such as the Carbon Offsetting and Reduction Scheme for International Aviation, known as CORSIA.

Global carbon pricing has grown steadily. Nearly 30 percent of global greenhouse gas emissions now sit under some form of direct carbon price. The World Bank’s 2026 State and Trends of Carbon Pricing report counts 87 separate policies worldwide. Notably, Indonesia sits among a group of large middle income economies moving from policy design to implementation. Brazil, India, and Turkey sit in this same group.

Why This Topic Matters Now

SRUK Launch and Indonesia’s Domestic Pivot

Indonesia’s carbon market moved from paper to practice this month. SRUK became operational on July 9, 2026, under Minister of Environment Regulation No. 10 of 2026, following a trial phase earlier in the year during which project developers could submit data ahead of full launch. The registry gives every carbon unit a lifecycle status. Specifically, a unit can carry a status of available, retired, suspended, or cancelled. The system also requires every transaction to appear on record within two working days. This single design choice tackles the biggest complaint international buyers have had about Indonesian carbon credits for years. In particular, buyers worried that the same tonne of carbon could get sold twice.

Three days before the registry launched, Indonesia granted its largest forestry carbon credit approval to date. The Forestry Ministry authorized more than 30 million tonnes of carbon dioxide equivalent. Three Forest Utilization Business Permit holders and one social forestry entity received this approval. The transaction carries an estimated value of roughly Rp5 trillion, or about US$277.5 million. The government expects it to generate close to Rp500 billion in non-tax state revenue, or roughly US$27.8 million.

Verra has confirmed it will issue at least 20 million tonnes of CO2 equivalent to three named Indonesian forestry projects under this new framework. These are the Katingan Peatland Restoration and Conservation Project in Central Kalimantan, the Sumatra Merang Peatland Project, and The Mayas Project. This is a meaningful detail. It shows an international standards body actively issuing credits under Indonesia’s reformed rules, not merely commenting on them from the sidelines. Verra and the Ministry of Forestry are also building a direct data connection between the Verra Registry and SRUK, which should reduce reconciliation friction for buyers who want both domestic and international assurance on the same credit.

These events did not happen by accident. Indonesia timed them together deliberately. The message to global investors was clear. The country had moved past policy design and into implementation. The Forestry Ministry has since gone further, establishing an Indonesia Forestry Carbon Hub as a standing collaboration platform for the sector. This suggests the government intends forestry to remain the market’s proving ground while energy and other sectors catch up.

The Singapore-Indonesia Article 6 Partnership as a Template

Indonesia and Singapore have advanced a bilateral carbon credit partnership under Article 6 of the Paris Agreement. A broader environmental cooperation pact covering climate and the circular economy surrounds this deal. The partnership matters well beyond the two countries involved.

Singapore has a carbon tax. It needs high quality offsets to help its own companies meet climate obligations. Indonesia has the forests, peatlands, and renewable energy potential to supply them. The corresponding adjustment mechanics built into this deal will likely become Indonesia’s template for other buyer countries. Japan, South Korea, and members of the European Union could follow.

For a foreign investor, the practical lesson is simple. Watch how the Singapore transaction executes, not just how officials announce it. The details of authorization, registry recording, and adjustment timing in this first deal will shape every bilateral agreement that follows.

Political and Policy Debates

Not everyone in Jakarta feels comfortable with the pace of change. A member of Commission XII urged the government to complete a full national carbon balance during a parliamentary hearing on July 6, 2026. The lawmaker wants this done before Indonesia expands international carbon sales further. The argument is straightforward. Indonesia should know precisely how much it can sell abroad without undermining its own Nationally Determined Contribution.

This is a healthy debate, not a red flag. Sophisticated investors should welcome this kind of scrutiny. After all, it reduces the risk of a future policy reversal driven by public backlash. A market that faces no internal criticism is often a market nobody has tested properly.

Regulatory Architecture

Domestic Architecture

Indonesia’s carbon framework rests on a stack of laws and regulations built up over a decade. Understanding the sequence matters more than memorizing each instrument alone.

Law No. 16 of 2016 ratified the Paris Agreement and created Indonesia’s transparency obligations. Then, Law No. 7 of 2021, the Tax Regulations Harmonization Law, established the legal basis for a carbon tax. Presidential Regulation 98 of 2021 then created Indonesia’s first comprehensive carbon economic value framework. Specifically, it covered carbon trading, carbon levies, and results based payments.

PR 98/2021 was groundbreaking at the time. It was also, in practice, insufficient. In practice, it struggled with international trading mechanics. It left gaps in monitoring and verification standards. As a result, it created uncertainty for investors trying to structure cross border deals.

Presidential Regulation 110 of 2025 replaced this earlier framework with something considerably more robust. It introduced Carbon Allocation and GHG Emission Quotas as new concepts. It created a Steering Committee, known locally as Komite Pengarah or Komrah, to provide policy direction and coordinate across ministries. The Coordinating Minister for Food Affairs chairs this committee. Critically, its membership spans two Coordinating Ministers and 17 ministries and agencies, making it the broadest inter-ministerial coordination mechanism Indonesia has ever established for carbon governance. The committee’s kick-off meeting was held in Jakarta on October 20, 2025, signaling that the new framework moved immediately from paper to institutional reality. OJK is also a formal member of this committee, aligning its financial market regulatory function directly with the broader carbon economic value mandate.

Two changes matter most for investors. First, Article 58 of the new regulation decouples carbon trading from Indonesia’s own NDC milestones, meaning trading can proceed before the country hits specific national targets, rather than waiting on them as the old regime effectively required. Second, Article 66 formally recognizes voluntary offset trading and gives companies the legal right to purchase carbon units for purposes outside compliance obligations. Most importantly for market participants, the new regulation eliminated the requirement for a Mutual Recognition Agreement between Indonesia and international carbon standards bodies. Approvals and transactions now flow through sectoral ministerial regulations and the integrated registry system instead.

This brings us to a question that confuses almost every foreign investor at first encounter. Indonesia actually operates two registries, not one. However, they serve different purposes.

The table below sets out the distinction clearly.

Table 1: SRN PPI vs SRUK

| Feature | SRN PPI | SRUK |

|---|---|---|

| Full name | National Registry System for Climate Change Control | Carbon Unit Registry System |

| Purpose | Records national mitigation and adaptation actions | Records and administers carbon units and trades |

| Level | NDC level, national accounting | Carbon Economic Value implementation level |

| Established under | Earlier climate change control framework | PR 110/2025, operationalized by MoE Reg. 10/2026 |

| Launch status | Operating since earlier framework | Became operational July 9, 2026 |

| Who must register | Government bodies tracking national actions | Any party issuing, holding, or trading carbon units |

A carbon tax and a carbon trading scheme are also two separate instruments. Even so, conflating them is a common and costly mistake. The carbon tax, established under Law No. 7/2021, is a fiscal measure. Specifically, it applies a price to emissions above a certain threshold. Carbon trading, governed by PR 110/2025 and its implementing regulations, allows companies to buy and sell verified emission reductions. A company might face carbon tax liability in one part of its operations. At the same time, that same company might simultaneously generate tradable credits in another part of its business. Legal advisors need to assess both exposures separately.

Sector by sector, the regulatory picture is uneven. Forestry sits furthest ahead. Here, Forestry Ministerial Regulations No. 6 and No. 7 of 2026 govern carbon trading procedures, environmental integrity standards, and investment certainty specifically for forestry projects. Energy sector rules remain under preparation. Currently, the government targets completion within one to two months of this writing. Waste management and industrial process sectors sit further behind still.

Transport offers a useful illustration of how far the market still needs to expand beyond forestry. Indonesia’s state railway operator has published a net zero roadmap targeting a 25.76 percent emissions cut by 2030, rising to full net zero by 2060, built around rail electrification and higher biodiesel blends. Road transport still accounts for roughly 89 percent of Indonesia’s transport emissions against rail’s roughly one percent, which shows both the scale of opportunity outside forestry and how early most non-forestry sectors remain in generating tradable credits.

International Linkages

Article 6 of the Paris Agreement is where Indonesia’s domestic reforms meet the global market. This is the section every foreign buyer should read most carefully.

Under PR 110/2025, any internationally linked carbon trade requires two things before execution. It needs authorization from the Minister of Environment. It also needs a completed corresponding adjustment procedure. This rule covers Article 6.2 transactions, Article 6.4 transactions, and voluntary offsets serving other international obligations. It is a deliberate control point. Indonesia’s government retains oversight of every credit leaving the country this way, rather than letting private parties transact freely across borders.

The corresponding adjustment itself works like an accounting entry between two national ledgers. Indonesia must subtract that same tonne from its own Nationally Determined Contribution accounting when it transfers a verified emission reduction to Singapore. Singapore adds that tonne to its own accounting in turn. Without this adjustment, both countries could claim credit for the same tonne of reduced carbon. Otherwise, that would overstate global progress on climate change.

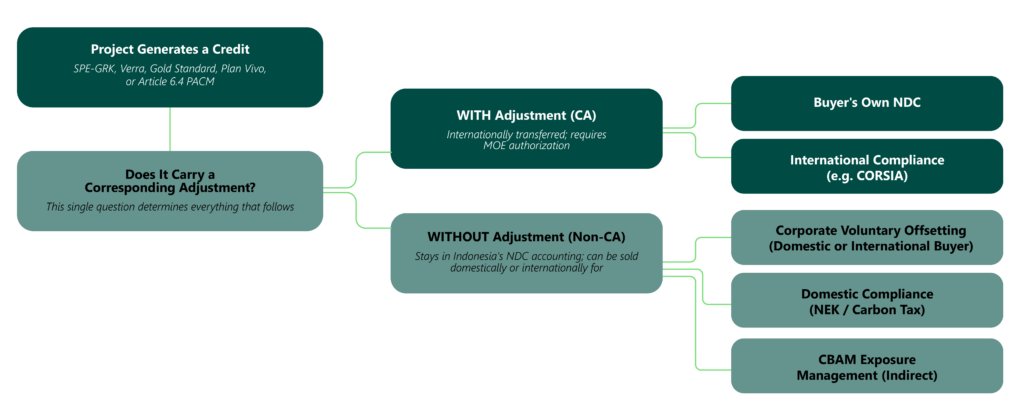

Figure 1 below sets out how a credit actually moves through this system, from an Indonesian project to a foreign buyer’s own climate accounting.

The removal of the Mutual Recognition Agreement requirement as a precondition for international trading matters for this same reason. Indonesia previously required a formal MRA with a standard such as Verra or Gold Standard before credits under that standard could move internationally with full legal certainty. That step no longer operates as a mandatory gateway. Authorization now flows directly through the sectoral ministry and the Minister of Environment. This route is faster. It also places more weight on Indonesia’s own institutional capacity to conduct rigorous review.

Importantly, removing the MRA precondition does not mean Indonesia has turned its back on MRAs as a governance tool. The government separately signed MRAs with Verra, Gold Standard, Plan Vivo, and the Global Carbon Council in 2025. These agreements now sit alongside the new authorization pathway rather than above it. The practical effect is a more flexible architecture: a project can proceed through direct ministerial authorization, and if an MRA is also in place with the relevant standard body, that adds an additional layer of assurance that buyers can rely on. Investors comparing credits should treat the existence of an MRA as a quality signal, not as a prerequisite.

Figure 2 below sets out the one decision that shapes everything about how an Indonesian credit reaches the market: whether it carries a Corresponding Adjustment or not. Everything downstream, from which buyer can use it to which compliance scheme will accept it, follows from this single fork.

How an Indonesian Carbon Credit Reaches the Market

Source: Depiction based on PR 110/2025 and Ministry of Environment Regulation No. 10/2026.

Figure 2: How an Indonesian Carbon Credit Reaches the Market

Sector coverage across Indonesia’s carbon market remains uneven. The table below, drawn directly from the Ministry of Environment’s own SRUK registry portal, sets out the six sectors now formally recognized under the Nilai Ekonomi Karbon framework, including Marine and Fisheries, a sector added under the current framework that earlier commentary on Indonesia’s carbon market often overlooked

| NEK Sector | What It Covers | Regulatory Maturity |

|---|---|---|

| Forestry | Forest and peatland based emission reductions, avoided deforestation, and carbon sequestration | Most developed; MoEF Regulations No. 6 and 7 of 2026 in force |

| Energy | Power generation, oil and gas, transportation, and building energy use and transformation | Sectoral rules under active preparation |

| Waste | Solid and liquid waste management activities that reduce CH4 and N2O emissions | Early stage |

| Industrial Processes and Product Use (IPPU) | Non-energy emissions from industrial and chemical processes and product use | Early stage |

| Agriculture | Low emission cultivation practices and enhanced carbon uptake across rice, livestock, and plantations | Early stage |

| Marine and Fisheries | Coastal and marine based emission reduction and sequestration activities | Newly recognized sector under SRUK; rules still emerging |

Table 2: NEK Sector Coverage (Source: Ministry of Environment, SRUK registry portal)

Forest certification is also entering this picture directly. The Forest Stewardship Council has partnered with Verra since May 2026 to label Verified Carbon Units generated from FSC certified forests, and it is developing a dedicated global carbon credit certification standard targeted for 2029 rollout, with explicit benefit sharing requirements for forest managers and Indigenous communities. For Indonesia, where FSC currently certifies roughly 4.5 million hectares of forest, this adds a further quality signal that buyers may increasingly expect alongside SRUK registration itself.

Institutional and Market Infrastructure

Several institutions now share responsibility for Indonesia’s carbon market. Knowing who does what saves significant time during a transaction.

The Steering Committee for Carbon Economic Value, called Komite Pengarah or Komrah, sits at the apex of the governance structure. As previously mentioned, it is chaired by the Coordinating Minister for Food Affairs, it draws membership from two Coordinating Ministers and 17 ministries and agencies, including the Ministry of Environment, the Ministry of Forestry, the Ministry of Energy and Mineral Resources, the Ministry of Finance, and Bappenas. OJK is also a member. This breadth reflects a deliberate design choice under PR 110/2025: carbon governance is not a single ministry’s problem. It is a whole-of-government coordination challenge.

The Ministry of Environment, known locally as KLH, oversees SRUK. It issues the authorizations required for international transfers. A separate but complementary body, the Badan Pengelola Dana Lingkungan Hidup or BPDLH, is the Environmental Fund Management Agency under the Ministry of Finance. BPDLH plays a critical and often overlooked role: it channels results-based payments, including REDD+ payments from the Green Climate Fund, to verified emission reduction projects across Indonesia. Investors in forestry and land-based projects who expect revenue through results-based payment mechanisms will transact with or through BPDLH rather than through the carbon exchange.

The Financial Services Authority, known as OJK, regulates the carbon exchange itself and the financial conduct of market participants. On July 6, 2026, OJK issued POJK No. 10 of 2026, updating its 2023 carbon trading regulation to align with PR 110/2025. The update formally integrates SRUK as the carbon unit registry, addresses international carbon trading procedures, and strengthens reporting and consumer protection requirements. This means the core financial regulatory framework for IDXCarbon is now current with the July 2026 market infrastructure launch.

A National Accreditation Committee, known as KAN (Komite Akreditasi Nasional), handles domestic accreditation for the independent validation and verification bodies that certify emission reduction projects. Under PR 110/2025, these verification bodies must be incorporated as Indonesian legal entities and hold either KAN accreditation or accreditation from an internationally recognized accreditation body. This is a tighter standard than the pre-2025 regime.

The Carbon Exchange and International Standards

IDXCarbon operates as Indonesia’s carbon exchange. This is the platform where verified credits get bought and sold. Since its September 2023 launch, more than 130 entities have joined the exchange. Four distinct trading mechanisms operate within it. Auction trading lets prospective buyers submit purchase requests with volume and price, with bidded units offered to the highest bidder. Regular trading operates as a continuous auction where all parties submit buy and sell offers. Negotiated trading settles pre-agreed deals struck outside the system. The marketplace mechanism lets project owners list units at fixed prices, giving them more control over their own sales strategy. The exchange must maintain an integrated interface with SRUK. Consequently, ownership records and transaction data update in something close to real time.

International standards bodies such as Verra and Gold Standard continue to play an important role. In particular, buyers who want an internationally recognized methodology layered on top of Indonesia’s domestic framework value them highly. Their formal recognition within the new system, alongside the removal of the old precondition for Mutual Recognition Agreements, already appears to be strengthening international confidence in Indonesian credits, as the Verra forestry issuance and the associated registry integration work demonstrate.

A Possible New Institution to Watch

A forward-looking development worth tracking: in late June 2026, Environment Minister Mohammad Jumhur Hidayat publicly raised the idea of establishing an independent statutory climate advisory body modelled on the United Kingdom’s Climate Change Committee. The concept, which emerged from a bilateral meeting between Indonesian and UK officials during London Climate Week, would create an institution capable of providing objective, science-based climate recommendations free from political interference. As of early July 2026, the proposal remains at the conceptual stage. No enabling legislation or formal institutional mandate has yet been issued. Investors should nonetheless monitor this development. If established, such a body would represent a significant further step in Indonesia’s institutional credibility, providing independent benchmarks against which government policy decisions on carbon market participation could be assessed.

Why This Is a CXO-Level Issue

Carbon markets rarely make it onto a board agenda as a purely environmental topic anymore. Four distinct pressures are converging in Indonesia’s case. Each deserves direct attention from senior leadership rather than delegation to a sustainability team alone.

Balance Sheet Exposure

Companies with significant land holdings now have a genuine path to monetize emission reductions. As a result, these companies can treat carbon credits as a new revenue line. This applies to forestry, agriculture, and extractive industries alike. They no longer need to treat environmental compliance purely as a cost center.

Trade Exposure

Exporters selling into the European Union face the Carbon Border Adjustment Mechanism. This mechanism effectively prices imported goods based on their embedded carbon. Access to credible, corresponding adjusted Indonesian credits offers one route to manage that exposure. Still, it does not eliminate the underlying need to decarbonize production itself.

Transactional Risk

Mergers and acquisitions involving Indonesian assets now require carbon liability and carbon asset due diligence as standard practice. This applies especially to forestry, agriculture, and energy deals. A target company holding unregistered or poorly documented carbon credits represents real legal risk to an acquirer. Fortunately, SRUK’s new double counting controls make this risk easier to spot, and harder to hide.

Consider a practical example. A regional agribusiness group is evaluating the acquisition of a plantation company in Kalimantan. The target holds forestry land with an existing peatland conservation area. Under the old framework, a buyer might have relied on the seller’s word that no carbon credits had been issued against that land. Under SRUK, a buyer’s legal team can check the registry directly. If the land already carries retired or sold carbon units, the buyer knows immediately that it cannot claim those same reductions again for its own sustainability reporting. This single check, which took days or weeks of correspondence before, now takes minutes. It is precisely the kind of operational improvement that turns a compliance headache into a competitive advantage for well advised acquirers.

Reputational Positioning

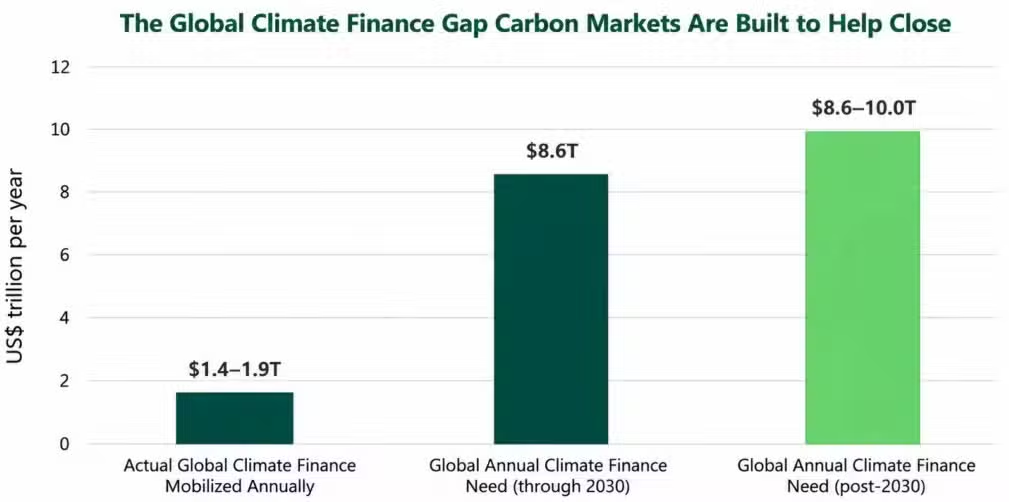

Global climate finance faces a genuine shortfall. Annual investment needs must reach roughly US$7.8 trillion a year through 2030, and climb further to US$9 trillion annually between 2031 and 2035, according to the Climate Policy Initiative’s Global Landscape of Climate Finance 2026 report. Actual global climate finance reached just over US$2 trillion in 2024, the first time flows have crossed that mark, though annual growth has slowed sharply since. Early, credible participation in a maturing market carries reputational value that a company cannot easily purchase once the market becomes crowded.

Boards and general counsels reviewing Indonesian investments should therefore ask direct questions. Is this asset’s carbon credit status registered in SRUK? Has anyone already sold or retired a credit associated with this asset? Does the counterparty hold proper sectoral ministry approval? These questions now belong on every standard due diligence checklist.

Data and Statistics

The numbers behind Indonesia’s carbon market tell a story of rapid scaling from a low base.

Table 3: Key Indonesian Carbon Market Figures

| Metric | Figure | Source |

|---|---|---|

| Forestry carbon credits approved / facilitated for issuance, July 2026 | Over 30 million tonnes CO2e | Ministry of Forestry, Indonesia |

| Verra-confirmed issuance across three named projects | At least 20 million tonnes CO2e | Verra, July 2026 |

| Estimated transaction value | Approximately Rp5 trillion (US$277.5 million) | Ministry of Forestry, Indonesia |

| Estimated non-tax state revenue generated | Approximately Rp500 billion (US$27.8 million) | Ministry of Forestry, Indonesia |

| SRUK transaction reporting requirement | Within 2 working days | MoE Regulation No. 10/2026 |

| IDXCarbon registered entities (since Sept 2023) | Over 130 entities | OJK / IDXCarbon |

| Global emissions under direct carbon pricing | Approximately 30 percent | World Bank, State and Trends of Carbon Pricing 2026 |

| Carbon pricing instruments implemented globally | 87 | World Bank, State and Trends of Carbon Pricing 2026 |

| Global annual climate finance need, 2025 to 2030 | US$7.8 trillion | Climate Policy Initiative, Global Landscape of Climate Finance 2026 |

| Global annual climate finance need, 2031 to 2035 | Up to US$9 trillion | Climate Policy Initiative, Global Landscape of Climate Finance 2026 |

| Actual global climate finance mobilized (2024) | US$2.008 trillion | Climate Policy Initiative, Global Landscape of Climate Finance 2026 |

These figures matter for two reasons. First, they show that Indonesia’s forestry sector alone can generate transaction volumes large enough to matter on a national fiscal scale. In other words, this is not just a corporate sustainability exercise anymore. Second, the figures underline a large gap. Global climate action requires far more funding than the world currently provides. In this context, credible emerging carbon markets like Indonesia’s exist specifically to help close that gap.

Figure 4: The Global Climate Finance Gap

Put these numbers side by side and a clear picture emerges. Indonesia’s single forestry issuance in July 2026 already represents a meaningful fraction of the country’s broader climate finance ambitions. If Indonesia can replicate this scale across additional sectors, starting with energy once those rules finalize, the country’s carbon market could grow into a genuinely significant contributor to closing the global climate finance gap. That said, scale alone does not guarantee quality. Investors should look for consistent growth in verified, registered, and properly adjusted transactions over the coming quarters, not just headline announcement volumes.

Investor Go-To Guide

For Foreign Investors: Offtake and Fund Perspective

Foreign investors approaching a carbon credit investment in Indonesia face a different set of questions than domestic developers do. Their questions center mainly on legal certainty and registry integrity. Domestic developers, in contrast, focus more on how to generate a project in the first place.

A foreign investor should confirm several things before committing capital. Start by checking the specific carbon unit’s registration status directly in SRUK. Status categories of available, retired, suspended, or cancelled determine whether a unit can legally transfer at all. Next, confirm whether the transaction requires a corresponding adjustment. If so, check whether Ministry of Environment authorization already exists or still needs approval. Then assess political risk honestly. The ongoing national carbon balance debate discussed earlier in this guide belongs in that assessment. Finally, understand what the removal of the MRA requirement really means. It shifts more responsibility onto direct engagement with Indonesian sectoral ministries. As a result, this changes the practical diligence process compared to older transactions structured before 2025.

Checklist: Foreign Investor Entry Steps

- Verify project registration and unit status directly in SRUK

- Confirm sectoral ministry approval chain for the specific project type

- Assess whether Article 6 corresponding adjustment applies to the intended use

- Review counterparty’s accreditation status with the National Accreditation Committee

- Structure transaction documentation to reflect the post-2025 regulatory regime, not the older PR 98/2021 framework

- Engage local counsel early, given the pace of regulatory change

For Domestic Developers and Corporates

Domestic developers face a more operational set of questions. Their focus sits on getting a project registered and generating revenue, not on cross border legal mechanics.

A developer with an existing or planned emission reduction project should first determine which sectoral ministry holds jurisdiction. Forestry, energy, waste, and industrial processes each answer to different regulatory tracks with different levels of maturity. Developers with project design documents already prepared should participate directly in SRUK. After all, the registry supports ongoing use rather than a one-time filing. Revenue recognition also deserves early attention from finance teams. Carbon credits sitting on a company’s balance sheet represent a new asset class. Consequently, this raises accounting questions that many Indonesian finance departments have not previously encountered.

Checklist: Domestic Developer Registration Steps

- Confirm sectoral ministry jurisdiction for the project type

- Prepare and submit project design documents

- Complete validation and verification through an accredited body

- Register the project and resulting units in SRUK

- Obtain sectoral ministry approval before any sale or transfer

- Establish internal accounting treatment for carbon credits as an asset class

Is Indonesia’s Carbon Market Investable Right Now?

This is the question every serious investor is actually asking, even when they phrase it differently. The honest answer has three parts.

The regulatory foundation stands considerably stronger today than it did even a year ago. PR 110/2025 closed real gaps. SRUK addresses the double counting problem that has undermined confidence in many developing country carbon markets historically. The removal of the MRA requirement shifts more responsibility onto Indonesian institutions. At the same time, it also removes a genuine source of delay for investors.

Real risks remain open at the same time. Energy sector rules are not yet final. As a result, investors focused on that sector face genuine regulatory uncertainty for the next one to two months at minimum. The national carbon balance debate remains unresolved. A future government decision to restrict international sales in favor of domestic climate targets stays a real possibility, however unlikely in the near term. SRUK itself started operating only days before we wrote this guide. Any new registry system carries some implementation risk in its first months, no matter how well designed it looks on paper.

Sovereignty concerns also deserve honest acknowledgment. Foreign participation in forestry and land based carbon projects touches directly on land rights, indigenous community consent, and national control over natural resources. Instead, they are political questions. They can shape public sentiment and, eventually, regulatory direction.

Our assessment draws on direct experience advising cross border transactions in Indonesia. The market rewards patient, well advised entry over speed. Investors who verify registry status, confirm sectoral approval, and structure transactions around the post-2025 regime hold a considerably stronger position. Those who move quickly on incomplete information, however, do not.

Partner Perspective

“I have spent the better part of the past decade advising clients on cross-border transactions involving Indonesian natural resources. Carbon credits are the newest and, in many ways, the most legally complex asset class I have seen emerge in that time. The complexity is not cosmetic. It runs through the ownership structure, the regulatory approval chain, the registry mechanics, and the question of what a buyer is actually acquiring when they purchase a credit.

What has changed in the past twelve months is not simply the rules. It is the seriousness with which Indonesia’s government is now enforcing them. SRUK is live. The forestry issuance of July 6 was not an announcement. It was a transaction. The Singapore partnership has a corresponding adjustment mechanism behind it, not just a political communiqué. These are material differences from where this market stood in last couple of years.

My honest assessment, speaking as a practitioner who has sat across the table from both buyers and developers in this market, is that the window for well-structured early entry is open now but will not stay open indefinitely. As more bilateral agreements follow Singapore‘s template and as energy sector rules finalize, the market will become both more liquid and more competitive.

The clients who are best positioned are not necessarily the ones who move fastest. They are the ones who get the legal architecture right the first time. That means registry verification, sectoral approval, corresponding adjustment clarity, and transaction documents that reflect the post-2025 regime. Those foundations take time to build properly. Starting that work now is the right call.”

Frequently Asked Questions

What is the difference between SRN PPI and SRUK, and do I need to register in both?

SRN PPI records Indonesia’s national climate mitigation and adaptation actions at the NDC level. SRUK records and administers actual carbon units and trades at the implementation level. In practice, most private companies transacting in carbon credits will primarily use SRUK. Government bodies and certain large emitters may carry obligations under both systems, depending on their role.

Is Indonesia’s carbon tax under Law No. 7/2021 actually being enforced, or is carbon trading the only active mechanism right now?

Both instruments exist under Indonesian law. However, carbon trading has seen more visible activity recently, given the SRUK launch and the July 2026 forestry issuance. The carbon tax applies as a fiscal measure to emissions above certain thresholds, separate from any trading activity a company might also undertake. Companies should assess both exposures independently. In short, neither instrument substitutes for the other.

Can a foreign company buy Indonesian carbon credits for its own NDC or CBAM compliance, and what is a Corresponding Adjustment?

Yes, subject to Ministry of Environment authorization and a completed corresponding adjustment. Specifically, this adjustment is an accounting mechanism. It ensures only one country claims credit for a given tonne of reduced emissions. Otherwise, both the selling and buying country could count the same reduction toward their respective climate targets, misrepresenting actual global progress.

What happened to the Mutual Recognition Agreement requirement under the old framework?

PR 110/2025 removed the requirement for a formal Mutual Recognition Agreement between Indonesia and international carbon standards bodies. Previously, credits were generally expected to have this agreement in place before they could move internationally. Authorization now flows through sectoral ministerial approval and Ministry of Environment sign-off directly. Overall, this route moves faster, though it places more emphasis on Indonesia’s own institutional review capacity.

What sectors can currently generate carbon credits in Indonesia, and which are still pending regulation?

Forestry stands as the most developed sector. Specifically, dedicated Ministerial Regulations No. 6 and No. 7 of 2026 support it directly. Energy sector rules remain under preparation, with completion targeted within one to two months of this guide’s publication. Waste management, transport, and industrial process sectors sit less developed still. Therefore, prospective investors in those areas should monitor them closely.

How does Indonesia prevent double counting or double selling of the same carbon credit?

SRUK assigns every registered carbon unit one of four status categories. These are available, retired, suspended, or cancelled. As a result, this structure stops a unit that has already sold or retired from getting sold again. Every transaction must appear in the registry within two working days. Consequently, the status stays current and auditable.

Is now a good time to invest, given the debate over Indonesia’s national carbon balance?

The debate reflects healthy regulatory scrutiny rather than a fundamental barrier to investment. Indonesia’s legal foundation stands materially stronger than it did before 2025. Real uncertainties remain around energy sector rules and how much surplus Indonesia can responsibly sell abroad. Patient, well advised investors hold the best position here. Those who verify registry status and sectoral approval before committing capital will navigate this transition most successfully.

The information provided here is for information purposes only and is not intended to constitute legal advice. Legal advice should be obtained from qualified legal counsel for all specific situations.

DFDL offers expert Energy, Natural Resources and Infrastructure solutions across 10 ASEAN jurisdictions. Explore our Indonesia team.