Tabled for its first reading in the Malaysian Parliament on 4 March 2025, the long awaited Consumer Credit Act 2025 (“Act”) came into force on 1 March 2026, together with the establishment of the Consumer Credit Commission (“Commission”). With the aim of protecting the interests of credit consumers in Malaysia, the Act seeks to bring order to a historically fragmented sector by:

- regulating all credit businesses and credit service businesses;

- ensuring proper conduct and responsible lending practices by credit industry participants; and

- promoting the development of a fair, efficient, and transparent credit industry.

This alert seeks to draw down on the key takeaways from the Act.

Key Dates

1 March 2026: Date of Act coming into force

1 June 2026: Date when licensing and registration requirements for credit business providers and credit service business providers take effect

1 June 2026 to 31 December 2026: Transition period for industry participants to apply for licences or registration under the Act

Scope of regulation

In addition to establishing the Commission, the Act authorises the Ministry of Housing and Local Government to appoint a registrar of Islamic credit providers (“Registrar”). The Regulatory and Supervisory Authority under the Act consists of the Central Bank of Malaysia, the Securities Commission of Malaysia, the Ministry of Domestic Trade and Cost of Living, the Ministry of Housing and Local Government, and the Malaysia Co-operative Societies Commission. These authorities will exercise regulatory and supervisory powers over credit providers and credit service providers in their respective sectors.

With the aim of improving consumer protection and to clamp down on unlicensed operators, the Act establishes a single framework covering a broad range of credit businesses and credit service businesses. It brings previously unregulated sectors within scope by requiring providers to obtain a licence or register before commencing operations1.

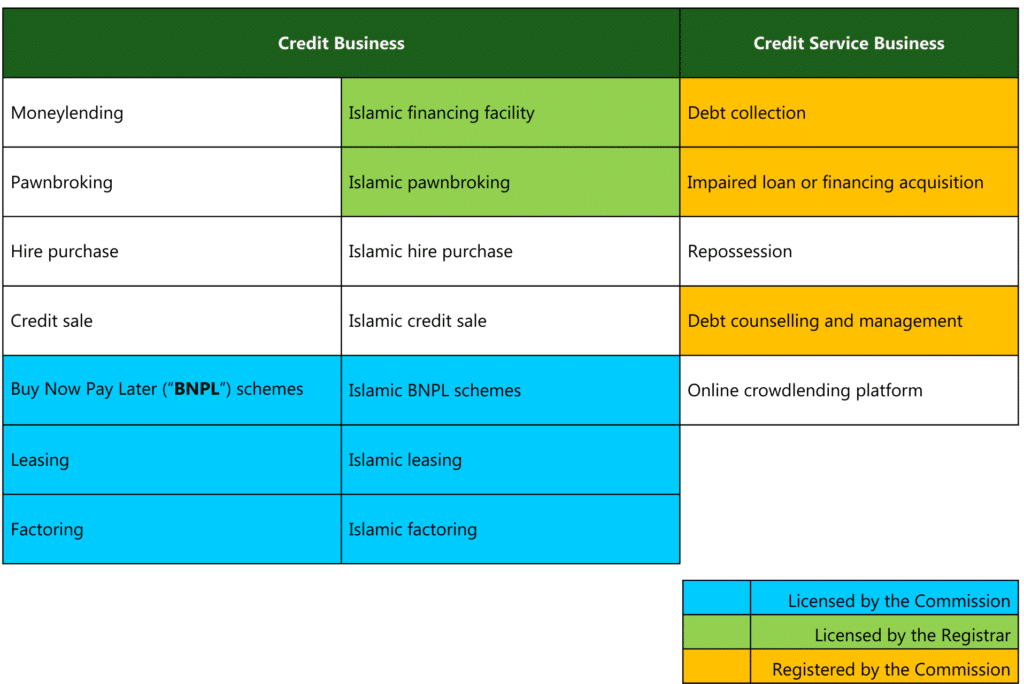

The following are credit business2 and credit service businesses3 regulated under the Act:

Licensing, registration and oversight

The Act sets out the licensing and registration eligibility of credit businesses and credit service businesses, which extends beyond entities themselves to cover the individuals responsible for their control and management. Where licensing or registration is required, credit business providers and credit service business providers will have six months to comply with the respective licensing and registration requirements under the Act once the rules take effect, according to the Ministry of Finance. The licensing rules take effect on 1 June 2026.

To qualify for and maintain a licence or registration, applicants must meet a prescribed minimum financial threshold at all times and demonstrate that their controllers, directors, and senior management are “fit and proper”. The fit and proper test addresses three elements: (a) probity, personal integrity and reputation; (b) competence and capability; and (c) financial integrity. Although detailed regulatory standards have yet to be prescribed, the earlier consultation paper suggests that the assessment will likely take into account an individual’s qualifications, experience, and track record, as well as any concerns relating to past misconduct, financial soundness, or reputational risks arising from their business associations.

In defining who falls within the scope of these requirements, the Act deliberately takes a substance-over-form approach. “Senior management” is defined broadly to capture any individual charged with managing part of the business or holding decision-making authority, regardless of title. Explicitly included are the chief executive officer and chief financial officer, though the scope is intended to encompass all real decision-makers. The concept of “controller” is also defined widely, echoing ultimate beneficial ownership frameworks. Controllers may include:

- shareholders who directly or indirectly hold at least 33% of the voting rights;

- those who have the power to appoint or influence the appointment of a majority of the board; or

- any person who has the power to make or cause decisions to be made regarding the business or its administration.

Where a controller fails to meet the fit and proper standard, the Commission has the power to require divestment of the relevant shareholding or for that person to otherwise cease exercising control within a prescribed period. The same principle applies to directors and senior managements who no longer meets the fit and proper standards. Further guidance is therefore critical for the industry to fully understand the operational and documentary requirements for licensing and ongoing compliance.

While licences and registrations under the Act are not subject to annual renewal, the Commission retains the right to revoke, suspend, or deregister a licence or registration in cases of non-compliance with the Act or its regulations, including non-payment of annual fees, failure to meet governance or reporting obligations, or failure of key personnel to maintain fit and proper status. This underscores the principle that regulation is an ongoing obligation, rather than a one-off approval.

Sale of credit service business

Under the Act, a registered credit service provider is required to obtain prior written approval of the Commission before it may sell, dispose, lease, assign or otherwise transfer the whole or any part of its credit service business to any other person; or amalgamate or merge its credit service business with any other person4.

Further, a registered credit service provider is prohibited under the Act from transferring or assigning its registration to any other person; or causing or permitting any other person to use its registration to carry on the credit service business specified therein5.

Consumer credit protection

The Act places a duty on credit providers and credit service provides to act in a fair, responsible, and professional manner. While the Act lays down the overarching obligation, the specific requirements are expected to be further detailed through regulations, guidelines, and sector-specific standards. These are anticipated to cover matters such as transparency and disclosure obligations, fairness of contractual terms, the imposition of interest, profit, fees or charges, advertising and promotional practices, fair debt collection standards, and measures to assist consumers facing financial hardship in meeting their obligations under a credit agreement. For sectors that were previously unregulated – such as debt collection, leasing services, and factoring services – this represents a fundamental shift, as they will no longer be free to impose terms unilaterally but must instead comply with a clear set of consumer protection requirements.

Another key safeguard under the framework is the requirement for non-bank credit providers to conduct affordability assessments before extending credit to individuals. Providers must ensure that borrowers have the financial capacity to fully repay their debts without suffering undue financial hardship over the duration of the credit facility. This measure is intended to promote responsible lending practices and to curb over-indebtedness, thereby strengthening consumer protection across the credit market.

Public Register of Licencees

Prior to the Act, members of the public who wish to verify whether a moneylender is properly licensed may do so by referring to the ikreditkom app. The Act now imposes a statutory obligation on the Commission to maintain and publish a list of all licensed credit providers and registered credit service providers under its purview6, thereby enhancing transparency and making it easier for consumers to identify legitimate, regulated operators.

BNPL under the Act

According to infographic published on the website of the Consumer Credit Oversight Board Task Force, BNPL has grown rapidly in Malaysia, with 140.4 million transactions worth RM12 billion recorded in the second half of 2025. As of the second-half of 2025, there were 7.5 million active BNPL accountholders, an increase from 5.1 million at the end of 2024. The total BNPL outstanding balance as at the second half of 2025 has grown to RM 4.9 billion, underscoring the need for stronger oversight.

To constitute a BNPL scheme, the Act requires for there to be “an arrangement, by whatever name called, entered into between a credit consumer and a third-party credit provider for the purchase of goods or services by the credit consumer from a seller where: (i) the third-party credit provider provides credit to the credit consumer; and (ii) the payment due by the credit consumer to the third-party credit provider is deferred and may be made in a single payment or by instalments in accordance with the terms and conditions of the arrangement.”

According to this definition, a BNPL scheme involves a tripartite arrangement comprising the buyer (credit consumer), the seller, and the credit provider (the entity providing the BNPL service). As such, if the credit is extended directly by the seller, such arrangements would technically not fall within the definition of a BNPL scheme under the Act. This distinction is important, as it separates BNPL arrangements from conventional credit sales, in which the extension of credit is intrinsically linked to the underlying sales transaction.

Conclusion

The Act is a significant first step towards bringing a broad range of previously unregulated sectors within a single, coherent regulatory framework. With regulatory guidelines and sector-specific standards to be issued, the full picture of compliance will continue to evolve. In the meantime, with licensing and registration requirements taking effect from 1 June 2026, industry participants should act promptly to assess their obligations, prepare for compliance and ensure that their governance and operational frameworks are ready for the new regulatory order.

The information provided here is for information purposes only and is not intended to constitute legal advice. Legal advice should be obtained from qualified legal counsel for all specific situations.

Footnotes